I can handle the truth just fine, thank you. You’re the one who is in near constant denial.

As for my day, my portfolio was pretty flat. Not bad, not good. But then I don’t get my undies all in a bunch over a single day like some people here.

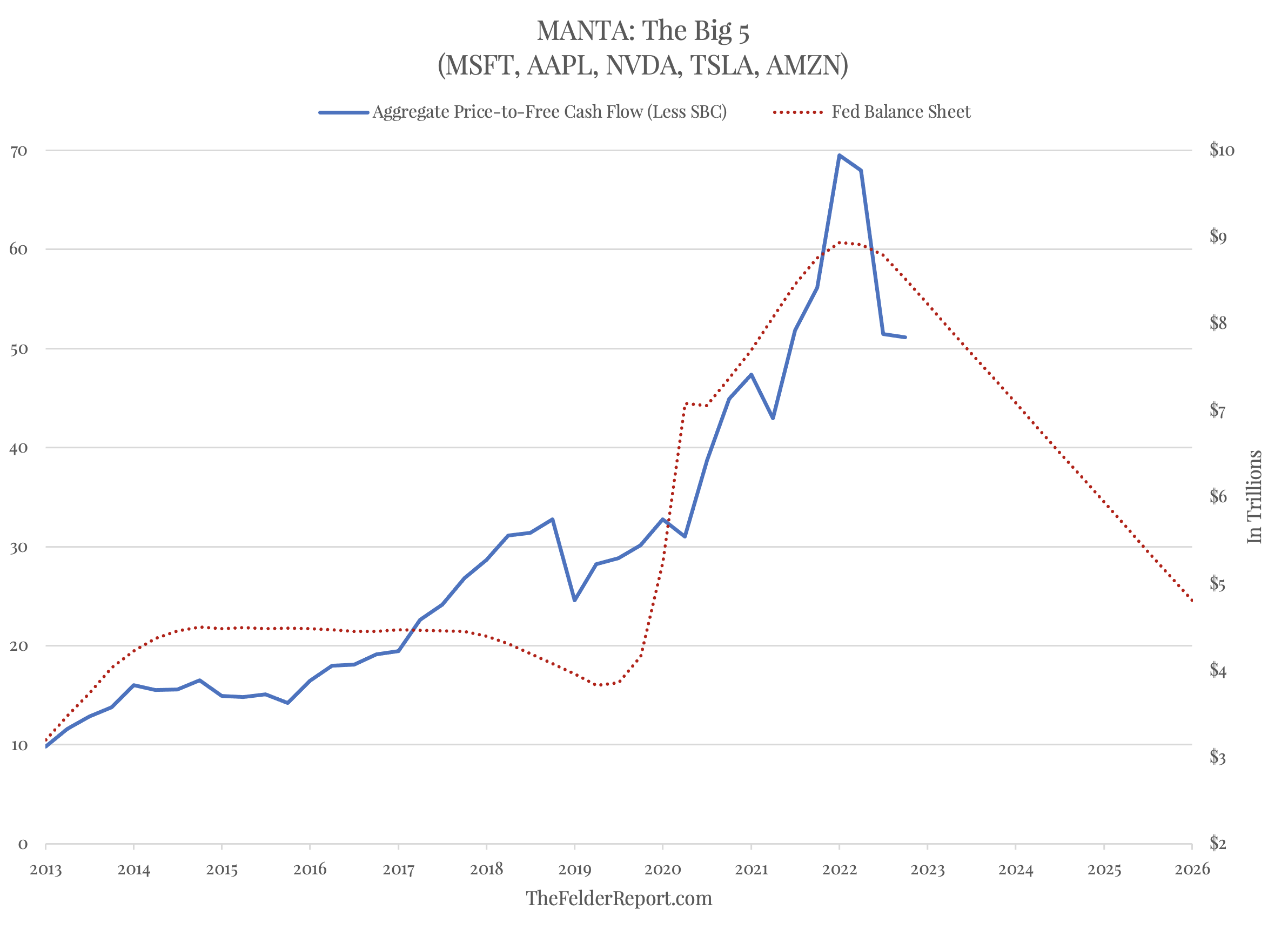

“Put the market caps together of Microsoft, Apple, Nvidia, Tesla and Amazon and compare that figure with their aggregate free cash flow and you get a multiple of over 50 times, down from nearly 70 at the start of the year. This historic level of overvaluation was only made possible by massive money printing on the part of the Fed that supported both cash flows and the multiple applied to them. Now that inflation is raging, however, the money printer has been shifted into reverse and that’s already having a visible impact (both “bearish forces,” the reversion in valuations and falling liquidity, have been consolidated into one chart this time below).”

MSFT and aapl are fundamentally different businesses than tsla and nvda, and also they trade at much more reasonable PEs. Tsla and nvda are skewing the comparison

MSFT and aapl are fundamentally different businesses than tsla and nvda, and also they trade at much more reasonable PEs. Tsla and nvda are skewing the comparison

“At the start of the month, the five largest components of the index (Microsoft, Amazon, Nvidia, Tesla and Apple, aka MANTA) traded at about 55-times their aggregate free-cash-flow (and nearly 70-times when you back out stock based compensation). Now that might not be totally obscene if it weren’t for the fact that free cash flow growth has recently turned negative. In that context, however, it’s hard to see how the most extreme valuation in the history of this group is at all sustainable.”

MSFT and aapl are fundamentally different businesses than tsla and nvda, and also they trade at much more reasonable PEs. Tsla and nvda are skewing the comparison

Current and historical p/e ratio for Microsoft (MSFT) from 2010 to 2022. The price to earnings ratio is calculated by taking the latest closing price and dividing it by the most recent earnings per share (EPS) number. The PE...

MSFT and aapl are fundamentally different businesses than tsla and nvda, and also they trade at much more reasonable PEs. Tsla and nvda are skewing the comparison

Current and historical p/e ratio for Apple (AAPL) from 2010 to 2022. The price to earnings ratio is calculated by taking the latest closing price and dividing it by the most recent earnings per share (EPS) number. The PE rati...

“The rises of social media platforms find many investors falling prey to dogma of fear driving pseudo economists and halfhearted investors. Some rather infamous purveyors of fear driven narratives include Sven Henrich and Jesse Felder. To be perfectly clear, Henrich and Felder’s narratives almost always portray the demise of equity markets and impending declines. They are almost always wrong and inherently leaning in favor of inevitability. We all know the market will decline, inevitably.”

In reviewing the year-to-date major indices rally, I can’t help but to think that many, many investors have suffered from being captive of the moment and missing the big picture. Being captive to the moment refers to the perv...

“The rises of social media platforms find many investors falling prey to dogma of fear driving pseudo economists and halfhearted investors. Some rather infamous purveyors of fear driven narratives include Sven Henrich and Jesse Felder. To be perfectly clear, Henrich and Felder’s narratives almost always portray the demise of equity markets and impending declines. They are almost always wrong and inherently leaning in favor of inevitability. We all know the market will decline, inevitably.”

^ :-) “Investors need to understand that China is a managed economy and that officials aren’t likely to stand by and let the world’s second-largest economy flounder and falter for too long before taking action. Stimulus has poured into the Chinese economy and found working already, akin to the vast amounts of stimulus poured into economies of scale in former years. Thus the Chinese equity markets have rebounded, as they should.”

“The rises of social media platforms find many investors falling prey to dogma of fear driving pseudo economists and halfhearted investors. Some rather infamous purveyors of fear driven narratives include Sven Henrich and Jesse Felder. To be perfectly clear, Henrich and Felder’s narratives almost always portray the demise of equity markets and impending declines. They are almost always wrong and inherently leaning in favor of inevitability. We all know the market will decline, inevitably.”

^ “Being captive to the moment refers to the pervasive negative sentiment that was born out of the Q4 2018 market sell-off. With the S&P 500 (SPX) falling some 20% from its peak to trough level, investors succumb to fear and the all-too formative loathing that has kept many investors on the sidelines and missing a great opportunity to either recapture former losses or gains from the 16% rally in the benchmark index.”

It wasn’t the great economy or equity market in 2019, it was the Fed dropping QT and reducing interest rates. Fake markets the last ten years. Mommy and Daddy supporting the lemonade stand. Low and behold it led to bad behavior.

Interesting factoid, FB down about 75% from the high, and down 45% over the last five years. And somehow that cannot be the market experience over the next year?

Interesting factoid, FB down about 75% from the high, and down 45% over the last five years. And somehow that cannot be the market experience over the next year?

2.6%. And it’s a smoke in mirrors number because we can’t draw down the SPR by 200 million barrels every quarter to make inflation look artificially low. The use of the SPR as a political ploy is an abomination.

Interesting factoid, FB down about 75% from the high, and down 45% over the last five years. And somehow that cannot be the market experience over the next year?

2.6%. And it’s a smoke in mirrors number because we can’t draw down the SPR by 200 million barrels every quarter to make inflation look artificially low. The use of the SPR as a political ploy is an abomination.

2.6%. And it’s a smoke in mirrors number because we can’t draw down the SPR by 200 million barrels every quarter to make inflation look artificially low. The use of the SPR as a political ploy is an abomination.

That and selling to Europe.

trying to defund Putin by lowering oil prices is a valid use of the SPR in proxy wartime. If an R did it you all would consider it next-level genius.

Anyway, solid GDP number today - not too hot, not too cold.

Big question is what GDP Now thinks 4Q will be. Most economists seem to think the economy will hit a slower patch over the next month or two.

Other big question is what the PCE inflation number is tomorrow...that one could move markets mightily and end this rally in a millisecond.

trying to defund Putin by lowering oil prices is a valid use of the SPR in proxy wartime. If an R did it you all would consider it next-level genius.

Anyway, solid GDP number today - not too hot, not too cold.

Big question is what GDP Now thinks 4Q will be. Most economists seem to think the economy will hit a slower patch over the next month or two.

Other big question is what the PCE inflation number is tomorrow...that one could move markets mightily and end this rally in a millisecond.

Except he's not doing it to defund Putin. He's doing it to make the economy look artificially "strong as hell" going into the midterms. There is a reason he did the release when he did (and didn't do things like reverse his executive orders hampering oil and gas production, which would have provided meaningful, longer-term relief from energy inflation). It would be like someone whose checking account has been steadily draining each month because their expenses have been exceeding their income suddenly boosting their balance by transferring money from savings. Yes, it makes their checking balance look better, but it hasn't solved the long-term problem that their expenses are higher than their income. All it did was decrease their savings.