Isn't cash always a store of value.

Isn't cash always a store of value.

Yes, and many learn that in a falling market.

I have heard a lot of negative rhetoric on cash over the last couple of years.

Ghost of Igloi wrote:

Yes, and many learn that in a falling market.

I have heard a lot of negative rhetoric on cash over the last couple of years.

Yes, Oh Wise One. What other astounding bits of wisdom do you have to share to save all of us fools?

Are not stocks also a store of value?

Yay $ U,

OK, buy stocks with both hands.

Igy

Say wha,

Not at these valuations. If you believe differently buy AMZN, NFLX, GOOG, FB and APPL.

Igy

Here's a more concrete question for ghost and others:

At what P/E would you make a significant index buy into the DJIA or SP500?

(by P/E, I mean index P/E)

Unbelievable,

I would say under 15.

Igy

coach d wrote:

Flagpole wrote:Again, what you wrote there could have been written by anyone on any day from the 1970s on, substituting some names of people and places and dates. In 1979 Businessweek had the article "The Death of Equities", and we have been told time and time again that stocks are not going to perform as they have (and I don't PLAN that they will), but then they find a way to do so. 1987, 1991, DOT COM bust, 2007-2009 crash, and since and before and in between.

Mutual funds have gained on average about 11% since inception which is right on what I have averaged yearly since 1989 when I started investing. I have a spreadsheet that projects earnings, and I have columns from 0% to 9%, so I don't even entertain 10% or 11% or more (even though history tells me I definitely could). So, I'm not PLANNING to get what I have gotten. The thing is though, so far I always expect a conservative return and over time I have always done better than I conservatively planned. Until there is a HUGE change in the way the US does business, there is no reason to expect a big change from what has happened. Companies still drive profits and value, and that is not likely to stop.

You're regurgitating exactly what the mutual fund industry wants you to think, and this is the major reason why my whole generation, except for people like me owning stocks, can't afford to retire. Many of the performance claims are so far off that you could be sued for malpractice if you were in business and claimed this.

The facts:

By Morningstar data, for the last 10 years, the average mutual fund return is 6%.

This site calculates the Compound Aggregate Return for the SP500:

http://www.moneychimp.com/features/market_cagr.htmIn constant dollars and with dividends reinvested, and return since 1871 is 7%. Seven percent. Not 10 percent or 11 percent or what charlatans like Dave Ramsey want you to think. But SEVEN percent.

And it can be worse than that. For the people I worked with before I retired in 2000, the return in constant dollars has been 1.91%.

Between 1969 and 1984, the return in constant dollars was 0.36%.

Because of this, the average return since 1970 is not even 7 percent. It is less than 6 percent.

The difference between the real 6 percent return since 1970 and the claimed 11 percent is SIX TIMES THE MONEY. Over 20 years, the difference is over TWO TIMES the money. And that's why most of my generation can't afford to retire.

Snake Oil.

10 years isn't long enough, brother, especially when it includes the worst meltdown since the Great Depression (other than the very-short lived 1987 thing). 11%+ is the number since inception. I have averaged right on that since I started in 1989. I don't even consider 11% going forward as my spreadsheet tops out at 9% for the most optimistic return. I count reinvested dividends and I don't adjust for inflation. I don't care too much about "real" returns. I just want the money to grow. One way you deal withj "real" returns is you make a sh!tpile of money and then retire with zero debt and OWN a house outright. House goes along with the market in price, Social Security goes along with inflation, and if you do the 4% rule (or even go to 3% if you must) you can raise that portion too by inflation increase. I've had a lot of people tell me since 1989 that the best days for investing were over and that I couldn't count on anything but paltry returns that would barely do enough to beat inflation. Well, that has not been my reality. I'm no genius at picking funds either. I have a bunch of different funds...large cap, small cap, mid cap, international, value, aggressive growth, and even some bonds for now. I add a little extra money in if I have it and the market has dropped a lot, but I've only done that less than 10 times since I started investing. Constant investing and diversity -- keys.

Ghost of Igloi wrote:

Unbelievable,

I would say under 15.

Igy

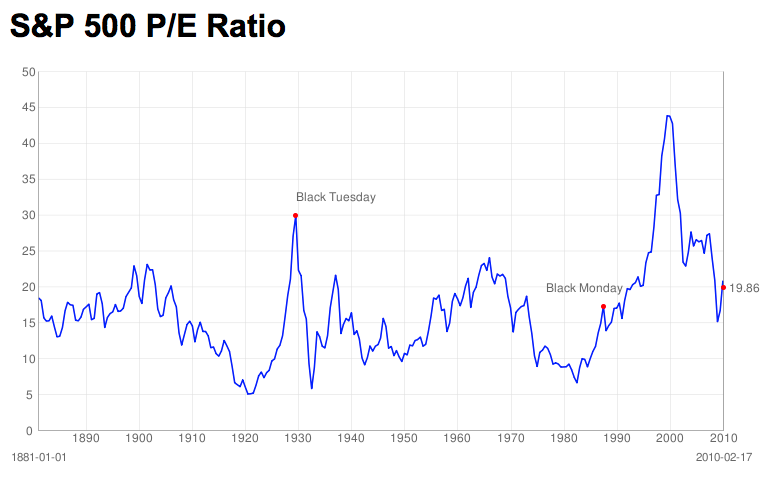

The trailing PE for the SP 500 hasn't been below 15 since the late 1980s.

Is it your feeling that people should have gone to cash in 1987 and not invested since? I'm being facetious here but the point stands - it is easy to make statements like that, but then you have the real world...

http://www.thedigeratilife.com/images/s-p-pe-ratio.pngagip wrote:

Ghost of Igloi wrote:Unbelievable,

I would say under 15.

Igy

The trailing PE for the SP 500 hasn't been below 15 since the late 1980s.

Is it your feeling that people should have gone to cash in 1987 and not invested since? I'm being facetious here but the point stands - it is easy to make statements like that, but then you have the real world...

http://www.thedigeratilife.com/images/s-p-pe-ratio.png

This is an exciting time for the market! If I had some extra coin today (don't because my daughter is about to start college), I would seriously consider putting in extra. Lots of FEAR right now (which is crazy when looking at the economy right now). Fear means time to strike! (though, that DOESN'T mean you should have been out of the market until now...you still stay in ALWAYS and only put in extra if you have it and have nothing else to do with it at the time).

Ghost of Igloi wrote:

http://www.multpl.com/

pretty much the same thing - by your chart there were two very short dips under 15. Does that change anything? Do you sell when the PE goes back above 15?

By 25 year averages, the market is just slightly expensive.

agip,

In my real world the last significant market correction was October 2011 during the first Greek crisis and the debt ceiling congressional crisis. PE then: Oct 1, 2011 13.88.

Igy

agip,

"By 25 year averages, the market is just slightly expensive."

True if you believe the numbers can be extrapolated into the future. I don't believe it for a second.

Igy

Ghost of Igloi wrote:

agip,

"By 25 year averages, the market is just slightly expensive."

True if you believe the numbers can be extrapolated into the future. I don't believe it for a second.

Igy

nah - just eyeball the chart of trailing 12 month PEs you yourself linked to - looks to me that the average trailing PE for 25 years is probably actually ABOVE where we are now.

I will say that 25 years is not a long time in the stock market and things can last 25 years and then go away.

agip,

I guess we will see how it plays out. Certainly the move in commodities and China leads me to be cautious. I also believe that it is interesting that many of the best performers today are high multiple stocks.

Igy

ROTFLMAO

Translation:

"I'M not going to invest more at this time, but YOU should."

Who cares if your daughter is "off to college"? What about that great ESA that you set up when your kid was born, and that you have been contributing to the whole time? Why the extra input now? Poor planning? Unforeseen costs? Changed circumstances?

You seem to be the champion of the standard model. What gives?

I almost believe you, because you could have said that you were buying in, and nobody could refute it. But given your posting history, I don't believe you. Please explain.

Brick House wrote:

ROTFLMAO

Translation:

"I'M not going to invest more at this time, but YOU should."

Who cares if your daughter is "off to college"? What about that great ESA that you set up when your kid was born, and that you have been contributing to the whole time? Why the extra input now? Poor planning? Unforeseen costs? Changed circumstances?

You seem to be the champion of the standard model. What gives?

I almost believe you, because you could have said that you were buying in, and nobody could refute it. But given your posting history, I don't believe you. Please explain.

1) I didn't say that YOU should invest more in the market now. I said that I would if I could. Investing EXTRA in the market is all about having money at the moment that you don't have a need for. I currently have a need for all of my non-retirement earmarked money.

2) You don't read my stuff if you think I set up an ESA. I haven't invested a single penny for my kids' education as far as any accounts go...and for my eldest, it has been a win for us that we didn't. We had some debt early on that we needed to clean up (and we have), and we decided that when the kids went to college we would just pay for it with our income. Well, that's what we will be doing. Elite colleges give extremely good financial aid based on need for families making even south of $150,000 a year. We make less than $150,000 a year, so it is cheaper for us to send our kid to this outrageously expensive college (if looking at list price) than to a state school. Just worked out that way. So, while we can afford to continue to invest in our retirement and not have to cut back an outrageous amount, and pay for her to go to college, we don't have extra (other than our emergency fund which I'm not touching) to put in the market at this time.

People get all bent out of shape over the cost of college. The only ones who really pay through the nose are the super wealthy who don't earn merit scholarships and the very poor who also don't earn merit scholarships (or admission to an elite college that gives great financial aid for those in need).

If you pay off debt before your kid goes to college, you can significantly limit your outgo so that you can pay for college with your income. State school and live at home, community college and then transfer, merit scholarships, admission to an elite college that gives great financial aid based on need (a need where you don't have to be poor either).

How is that a win? If you had some debt early on that you paid off before this year, how has it not been to your advantage to put money into the tax-free ESA account? It's the same logic you use when trying to convince the others of the merit of your way of investing. Put money into it as early as you can, and build it up. It would not have affected your eligibility for financial aid, which is predicated on income. The cumulative tax savings would likely have you further ahead than you are now, or than you will be in the coming years. At least that is the standard mantra.

Private vs public, scholarships, that's irrelevant to this discussion. The issue is not whether or not you can pay for it, the issue is how much you will end up paying for what you get. And you will end up paying more than you need have.

A poor investment decision on your part.

Fair or foul: Eurosport Olympic swimming announcer fired on the spot - for making a joke?

What? Track and Field New picks Nuguse 3rd - Hocker 9th in Olympic 1500?

2024 College Track & Field Open Coaching Positions Discussion

I went to The States; everyone had "F350" trucks we don't have in the UK

So they had a guy with one of his nuts hanging out by a kid at the opening Ceremony.....

Does anyone really want to see any more of Simone Biles? Come on - no one does!

{kind=link}