what exactly is it the take-away you want to impart here?

A lot of investors cannot afford your indifference. Nor could they withstand significant depreciation of their retirement funds from a prolonged bear market. For that matter, a lot of people don't even have retirement funds.

Do they not matter or do you just want to impress us with your good fortune?

1) Igy was commenting about MY investments, so I told him how concerned I was, which is not at all.

2) Investment discussion can't involve those who don't invest. I can't help them.

3) What is your definition of a prolonged bear market? 3 years? 5 years? 10 years? The latter is extremely unlikely. If a person with a normal-sized retirement account ($1-$3 million) wants to protect themselves against a lengthy bear market, they should do all these things: don't retire until you are debt free and own your house free and clear, have 3 YEARS of expenses saved in cash or other liquid way. That's pretty much it. If the market tanks a ton, you can use your 3 years of expenses to help pay for things while you wait for the market to recover. IF during that time you also have Social Security, then your 3 years of expenses will last even longer, maybe up to 5 years. If you get to the end of 5 years and the market hasn't recovered, well, at a minimum you have 5 fewer years you need to withdraw from your retirement pile. That's good enough for most people. If you have less than $1 million or even nothing or next to nothing, then you should plan to work until you are debt free and maybe until you are 70 and not start taking SS until then.

Is 1-3 million even enough to retire nowadays? You can't even buy a house for 1 million in many desirable areas now. My house is worth over 1 million and it's over 40 years old! Our net worth is around 1.3-1.4 million (not for long if the market tanks) but I feel like we won't be able to retire for another 20+ years.

1) Igy was commenting about MY investments, so I told him how concerned I was, which is not at all.

2) Investment discussion can't involve those who don't invest. I can't help them.

3) What is your definition of a prolonged bear market? 3 years? 5 years? 10 years? The latter is extremely unlikely. If a person with a normal-sized retirement account ($1-$3 million) wants to protect themselves against a lengthy bear market, they should do all these things: don't retire until you are debt free and own your house free and clear, have 3 YEARS of expenses saved in cash or other liquid way. That's pretty much it. If the market tanks a ton, you can use your 3 years of expenses to help pay for things while you wait for the market to recover. IF during that time you also have Social Security, then your 3 years of expenses will last even longer, maybe up to 5 years. If you get to the end of 5 years and the market hasn't recovered, well, at a minimum you have 5 fewer years you need to withdraw from your retirement pile. That's good enough for most people. If you have less than $1 million or even nothing or next to nothing, then you should plan to work until you are debt free and maybe until you are 70 and not start taking SS until then.

Is 1-3 million even enough to retire nowadays? You can't even buy a house for 1 million in many desirable areas now. My house is worth over 1 million and it's over 40 years old! Our net worth is around 1.3-1.4 million (not for long if the market tanks) but I feel like we won't be able to retire for another 20+ years.

Living up to your handle. The S&P500 returns roughly 10% per year on average, so if you have 1 million dollars in it, you're making $100,000/year passively, so even if you spend $100k/year, you'll never even begin dipping into your principal. At 3 million, you're making $300k/year. So you're basically asking if it's possible to live on $300k/year, which for most people is yes.

what exactly is it the take-away you want to impart here?

A lot of investors cannot afford your indifference. Nor could they withstand significant depreciation of their retirement funds from a prolonged bear market. For that matter, a lot of people don't even have retirement funds.

Do they not matter or do you just want to impress us with your good fortune?

Also, any good fortune I have is because I made it happen. I invested early and often and unbroken since 1989.

okay, apparently i took your comment out of context, and that in part explains my consternation,.

But good for you.

There's a boatload of people out there that didn't have your opportunities and breaks and good fortune, and they are not going to be so indifferent to seeing what little they have in the way of retirement savings get shredded.

Is 1-3 million even enough to retire nowadays? You can't even buy a house for 1 million in many desirable areas now. My house is worth over 1 million and it's over 40 years old! Our net worth is around 1.3-1.4 million (not for long if the market tanks) but I feel like we won't be able to retire for another 20+ years.

Living up to your handle. The S&P500 returns roughly 10% per year on average, so if you have 1 million dollars in it, you're making $100,000/year passively, so even if you spend $100k/year, you'll never even begin dipping into your principal. At 3 million, you're making $300k/year. So you're basically asking if it's possible to live on $300k/year, which for most people is yes.

Thanks. What about those people that retired this year? Say they retired with 1 million at the top in January. If you had 1 million on January 4, that'd be worth 862k today. After tax that's like 600k. So much for not touching your principal!

Thanks. What about those people that retired this year? Say they retired with 1 million at the top in January. If you had 1 million on January 4, that'd be worth 862k today. After tax that's like 600k. So much for not touching your principal!

If someone is retiring with $1M in savings, hoping to make that last a couple of decades or more, it’s probably not a great idea for that money to be sitting in equities. That seems pretty obvious, but perhaps not to everyone. My two cents, anyway.

An entire generation of entrepreneurs & tech investors built their entire perspectives on valuation during the second half of a 13-year amazing bull market run. The "unlearning" process could be painful, surprising, & unsettling to many. I anticipate denial. Some thoughts:

If someone is retiring with $1M in savings, hoping to make that last a couple of decades or more, it’s probably not a great idea for that money to be sitting in equities. That seems pretty obvious, but perhaps not to everyone. My two cents, anyway.

So you buy bonds and CDs that you have to hold for several years to get a 3% return while inflation is 7%?

If someone is retiring with $1M in savings, hoping to make that last a couple of decades or more, it’s probably not a great idea for that money to be sitting in equities. That seems pretty obvious, but perhaps not to everyone. My two cents, anyway.

Even if you have most of it in bonds, you'd be down, only slightly less than if you have most in equities. People also have a large share of net worth in their house(s), and we're now in the beginning stages of a housing bear market. I think I heard some stat that around 1/4 of "retired" people still owe a mortgage, funny as that seems.

If someone is retiring with $1M in savings, hoping to make that last a couple of decades or more, it’s probably not a great idea for that money to be sitting in equities. That seems pretty obvious, but perhaps not to everyone. My two cents, anyway.

So you buy bonds and CDs that you have to hold for several years to get a 3% return while inflation is 7%?

I guess YOU do whatever you think makes sense. If I were retiring with $1M in savings, I personally wouldn’t be staking it all on red at the roulette wheel…

Living up to your handle. The S&P500 returns roughly 10% per year on average, so if you have 1 million dollars in it, you're making $100,000/year passively, so even if you spend $100k/year, you'll never even begin dipping into your principal. At 3 million, you're making $300k/year. So you're basically asking if it's possible to live on $300k/year, which for most people is yes.

Thanks. What about those people that retired this year? Say they retired with 1 million at the top in January. If you had 1 million on January 4, that'd be worth 862k today. After tax that's like 600k. So much for not touching your principal!

You would have to be peak idiot to cash out 100% of your holdings for no reason, especially when the market is down more than 10% from recent highs. Assuming the person in your example has literally zero money elsewhere, they will need to cash out only enough to live on right now, which they should do month by month, so, like several thousand dollars per month. This will not eat into your principal at all as long as you're cashing out less than 86k/year, which should be absolutely zero problem for anyone who has been financially smart enough to retire with a million dollars.

So you buy bonds and CDs that you have to hold for several years to get a 3% return while inflation is 7%?

I guess YOU do whatever you think makes sense. If I were retiring with $1M in savings, I personally wouldn’t be staking it all on red at the roulette wheel…

Your analogy indicates you know essentially nothing about investing, markets, anything. The S&P 500 returns 10% per year on average, meaning you win every year (on average). The odds of winning on red at the roulette wheel are less than 50%, so you lose every play (on average). Equating the too is ignorant and incorrect at best.

Anyone who plans on living another 10+ years can feel totally fine about having a lot of their money in a broad market index fund. If you're really worried about short term fluctuations you can park your money in an I bond (currently yielding around 7%). If you're putting your money in savings or CDs, you are simply financially stupid/ignorant. It's really that simple.

If someone is retiring with $1M in savings, hoping to make that last a couple of decades or more, it’s probably not a great idea for that money to be sitting in equities. That seems pretty obvious, but perhaps not to everyone. My two cents, anyway.

It should not all be sitting in equities, but certainly most of it should be. Why miss out on the historically significant growth that you would see over decades?

I guess YOU do whatever you think makes sense. If I were retiring with $1M in savings, I personally wouldn’t be staking it all on red at the roulette wheel…

Your analogy indicates you know essentially nothing about investing, markets, anything. The S&P 500 returns 10% per year on average, meaning you win every year (on average). The odds of winning on red at the roulette wheel are less than 50%, so you lose every play (on average). Equating the too is ignorant and incorrect at best.

Anyone who plans on living another 10+ years can feel totally fine about having a lot of their money in a broad market index fund. If you're really worried about short term fluctuations you can park your money in an I bond (currently yielding around 7%). If you're putting your money in savings or CDs, you are simply financially stupid/ignorant. It's really that simple.

That is a lame post. The 22 year return from the peak of the Tech Bubble 3/2000 through 3/2022 (All Everything Bubble) the annualized S&P 500 return was 4.984% and with dividends reinvested ( which is rarely done as a practical matter) 6.944%. There has never in history been a period where the return was consistently 10% a year for a retiree.

Living up to your handle. The S&P500 returns roughly 10% per year on average, so if you have 1 million dollars in it, you're making $100,000/year passively, so even if you spend $100k/year, you'll never even begin dipping into your principal. At 3 million, you're making $300k/year. So you're basically asking if it's possible to live on $300k/year, which for most people is yes.

Thanks. What about those people that retired this year? Say they retired with 1 million at the top in January. If you had 1 million on January 4, that'd be worth 862k today. After tax that's like 600k. So much for not touching your principal!

Where are you getting a $262,000 tax burden on $862,000? That is waaayyy off.

Your analogy indicates you know essentially nothing about investing, markets, anything.

Haha, I love it. OK, think what you will. You're obviously smarter, more experienced, better educated and more knowledgeable than me. I recognize your internet superiority and bow before your enhanced intellect and insights. :-D

I've got skin in the game and this scenario (being close to retirement) is very real to me. I've looked at various combinations and permutations of end of career scenarios very carefully. You are welcome to consider me an idiot; in fact that is my old (now retired) fake name.

Your analogy indicates you know essentially nothing about investing, markets, anything. The S&P 500 returns 10% per year on average, meaning you win every year (on average). The odds of winning on red at the roulette wheel are less than 50%, so you lose every play (on average). Equating the too is ignorant and incorrect at best.

Anyone who plans on living another 10+ years can feel totally fine about having a lot of their money in a broad market index fund. If you're really worried about short term fluctuations you can park your money in an I bond (currently yielding around 7%). If you're putting your money in savings or CDs, you are simply financially stupid/ignorant. It's really that simple.

That is a lame post. The 22 year return from the peak of the Tech Bubble 3/2000 through 3/2022 (All Everything Bubble) the annualized S&P 500 return was 4.984% and with dividends reinvested ( which is rarely done as a practical matter) 6.944%. There has never in history been a period where the return was consistently 10% a year for a retiree.

But that's only true for the sum that you happened to invest in 3/2000. If you've been DCAing into an S&P500 index fund every week for the last 22 years you've done a hell of a lot better than a 5% return.

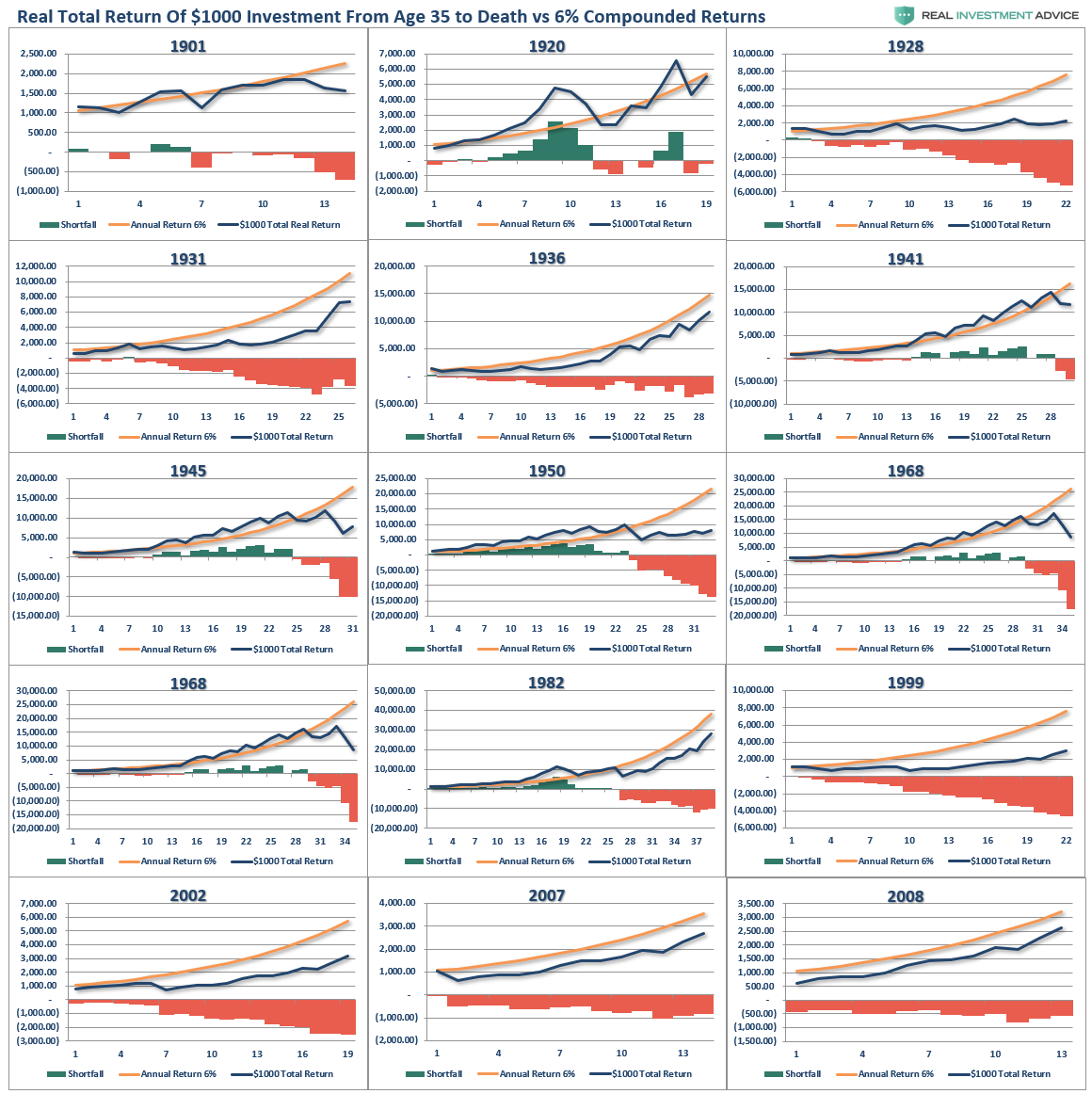

Igy - this is ridiculous even for you. All the charts you posted was for a date right before a precipitous decline in the market. Come on man - do better. Don't be deceitful. I am embarrassed for you to pull this stuff. The market HAS returned 11% annually for as long as it has been around. Please don't pick 2000 as a starting point. Try to be objective.

That is a lame post. The 22 year return from the peak of the Tech Bubble 3/2000 through 3/2022 (All Everything Bubble) the annualized S&P 500 return was 4.984% and with dividends reinvested ( which is rarely done as a practical matter) 6.944%. There has never in history been a period where the return was consistently 10% a year for a retiree.

But that's only true for the sum that you happened to invest in 3/2000. If you've been DCAing into an S&P500 index fund every week for the last 22 years you've done a hell of a lot better than a 5% return.

Igy chose 3/2000 because the market crashed after that and the S&P lost about 46%. He always picks that year because it puts the market in a bad light when instead the market has been, by far, the best investment vehicle bar none. Igy will always choose that year. It could not be more misleading.

Igy - this is ridiculous even for you. All the charts you posted was for a date right before a precipitous decline in the market. Come on man - do better. Don't be deceitful. I am embarrassed for you to pull this stuff. The market HAS returned 11% annually for as long as it has been around. Please don't pick 2000 as a starting point. Try to be objective.

Just a cursory look at the charts makes your criticism suspect.