This. House prices are stable right now, just not a lot of houses selling.

When interest rates drop, house prices will go up another 15-25%.

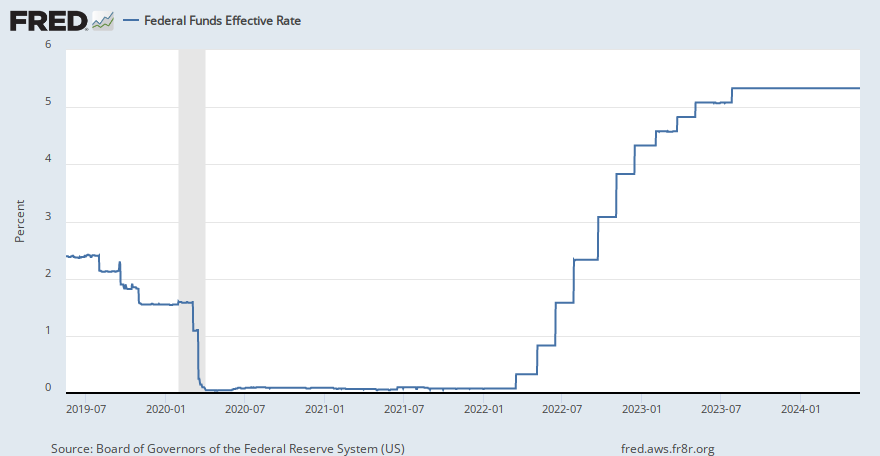

I'm a bull on RE and american in general, but why would housing prices go up if interest rates drop? Only way interest rates drop is if the economy starts to cool and more likely crash because the FED tends to be more reactive than proactive. I get that properties become more affordable (on a monthly basis), but there is likely less money sloshing around. No historical data to support interest rate drops leading to spike in housing prices happened once in 2020 which was all around weird.

What if we just built more houses to increase supply? From the 50s through to 2007, we built a . We've built almost none recently. People now refuse to allow new housing to get built near them because it'll lower their property values. Homeowners LOVE how high housing prices are getting.

In my area, you have to pay 30-50k over market value. Most people can't do that.

Market value is what people will pay for it. If houses go for 30-50K over what you believe market value is, then you're calculation of market value is 30-50K off.

Our population is increasing and housing is not keeping up. This isn't a bubble, it's a legitimate shortage which is driving prices up.

The problem is that Wall Street/private equity are paying way over market value to buy single family homes then turning around and renting those homes to families that got outbid.

They are FORCING us into becoming permanent renters so they can profit. They get the appreciation of the property and they collect massive rent payments.

In my area, you have to pay 30-50k over market value. Most people can't do that. The government needs to pass laws to stop this, but they are all owned by Wall Street.

First of all Wall Street generally refers to investment banking which isn’t the type of firm that buys residential real estate. Second, why would they intentionally “overpay”? Seems like a horrible investment thesis. Third, if you look at the data large commercial investors actually buy a very small percentage of existing residential RE inventory, especially SFHs. Fourth, if you’d like the government to mandate who can purchase and own what, maybe you should build a time machine and try living in the USSR, and perhaps you will learn some appreciation for living in a free market economy.

If housing prices correct 25% you won't be buying anything anyways, as you'll be out of a job.

I don't think you people understand the implication of a housing market crash. If you are in a place in your life where you can't afford a house now you are the most vulnerable when the economy crashes.

Get it together.

whether you lose your job in a recession depends on what kind of job.

If you have nothing to lose but your job, and do, the worst that will happen is the government supports you until the economy recovers. Meanwhile, few to no rent increases, little to no inflation.

House prices will sink. Mark my words. Look at a historical graph of (1) median income (2) median house price. The two lines shadow each other than a few brief periods where (2) bulges above (1) and then comes back. The current bulge is much, much bigger than any before it. The correction will therefore be bigger than ever before. The only thing that's unclear is whether the correction will be a big crash (down 10-25%/year for 1-2 years) or whether it'll just gradually go down for a decade or maybe stay flat while incomes catch up. Either way, it will have a big effect on the economy because most households have practically all their net worth tied up in their house.

The Wealth Effect is a real thing. The recent (The exact time it started was different depending on the area of the country) runup in house prices made people feel wealthy and caused them to spend more money. Now we'll see the reverse of that.

House prices will sink. Mark my words. Look at a historical graph of (1) median income (2) median house price. The two lines shadow each other than a few brief periods where (2) bulges above (1) and then comes back. The current bulge is much, much bigger than any before it. The correction will therefore be bigger than ever before. The only thing that's unclear is whether the correction will be a big crash (down 10-25%/year for 1-2 years) or whether it'll just gradually go down for a decade or maybe stay flat while incomes catch up. Either way, it will have a big effect on the economy because most households have practically all their net worth tied up in their house.

The Wealth Effect is a real thing. The recent (The exact time it started was different depending on the area of the country) runup in house prices made people feel wealthy and caused them to spend more money. Now we'll see the reverse of that.

A historical graph does not apply when there is no inventory. This is a pretty simple lesson in supply and demand.

The problem is that Wall Street/private equity are paying way over market value to buy single family homes then turning around and renting those homes to families that got outbid.

They are FORCING us into becoming permanent renters so they can profit. They get the appreciation of the property and they collect massive rent payments.

In my area, you have to pay 30-50k over market value. Most people can't do that. The government needs to pass laws to stop this, but they are all owned by Wall Street.

I follow homes in my area on Zillow and about a third or more of the sales for homes are cash and going up for rent right away.

How can you tell on the Zillow sales history that someone paid cash?

I know it's not personal. But I refuse. I'll wait until I can pay cash or the housing prices correct down 25%.

You may say these prices are low but I'm in a very low COL area with meager salaries, and taxes are about $7-9k/year. So it's not affordable at all.

Then ... don't.

I have a home in a VHCOL, but I bought small before the pandemic hit. I could upgrade, but it would bring about some unnecessary stress. My hope is to buy a townhome later outright in a lower COL area with some kind of freeze on the taxes for the olds.

I refuse to pay $300k for houses bought for $130k in 2018

That's cute. Where I am, you can't remotely buy even a zero-bedroom "condo" for $300. One bedroom condos start at $1 million, and actual houses are over $2 million for an old three-bedroom.

You can feel fortunate that you live in terrible city, I guess.

I know it's not personal. But I refuse. I'll wait until I can pay cash or the housing prices correct down 25%.

You may say these prices are low but I'm in a very low COL area with meager salaries, and taxes are about $7-9k/year. So it's not affordable at all.

People have been saying this since 2012 and prices have at least doubled in most decent areas, if not tripled. So even if prices went down 25% tomorrow, they'd be back at where they were in 2019, and most people were complaining about high housing prices back then as well.

Our population is increasing and housing is not keeping up. This isn't a bubble, it's a legitimate shortage which is driving prices up.

It's insanely expensive to build now between material/labor cost, permits, not to mention hassles with NIMBYs and other special-interest groups. The only construction I've seen in my area in the last 3-4 years has been massive "luxury" apartment complexes. Very few single family homes and townhouses.

Also, 8-10% interest rates were pretty standard in the 1990s and were much higher in the 1970s-1980s.

It's been proven that the best thing you can do is to buy a house when you need it and when you plan to live in it long term. Don't try to time the market. Don't buy a house now in case prices go up later. Don't be a miserable renter because you're gambling that prices will go down in a few years. An extra $20k in price shouldn't be a dealbreaker over a 30-year mortgage. If it is, you're probably not in a position to buy yet. Good luck.

This sounds so much like what I said in 2006 when I bought my first house. At that time, I couldn't imagine prices dropping. I bought a house for 300K, and within 2-3 years, it lost 60% of its value. I was finally able to sell it in 2019 at a small profit, but buying that house was the most financially catastrophic decision of my life.

I put 30% down, didn't lose my job and my salary and had a fixed rate mortgage. If you must buy now, I strongly suggest putting AT LEAST 10% down, not buying beyond what you can afford, and getting a fixed rate mortgage. If rates go down, you can refinance.

But I also wouldn't be surprised if we see a significant correction. I certainly wouldn't be in a rush to buy a house right now.